The Holy Grail of Risk-Free Trading

In traditional finance, true arbitrage is considered the Holy Grail. It is the simultaneous purchase and sale of an asset to profit from an imbalance in the price. It is, mathematically, a risk-free trade.

In cryptocurrency markets, the sheer number of trading pairs creates a unique phenomenon known as Triangular Arbitrage (TriArb). This occurs when the exchange rates between three different cryptocurrencies do not perfectly align, creating a temporary "loop" where money can be multiplied simply by converting it through the three assets.

The Mathematical Loop

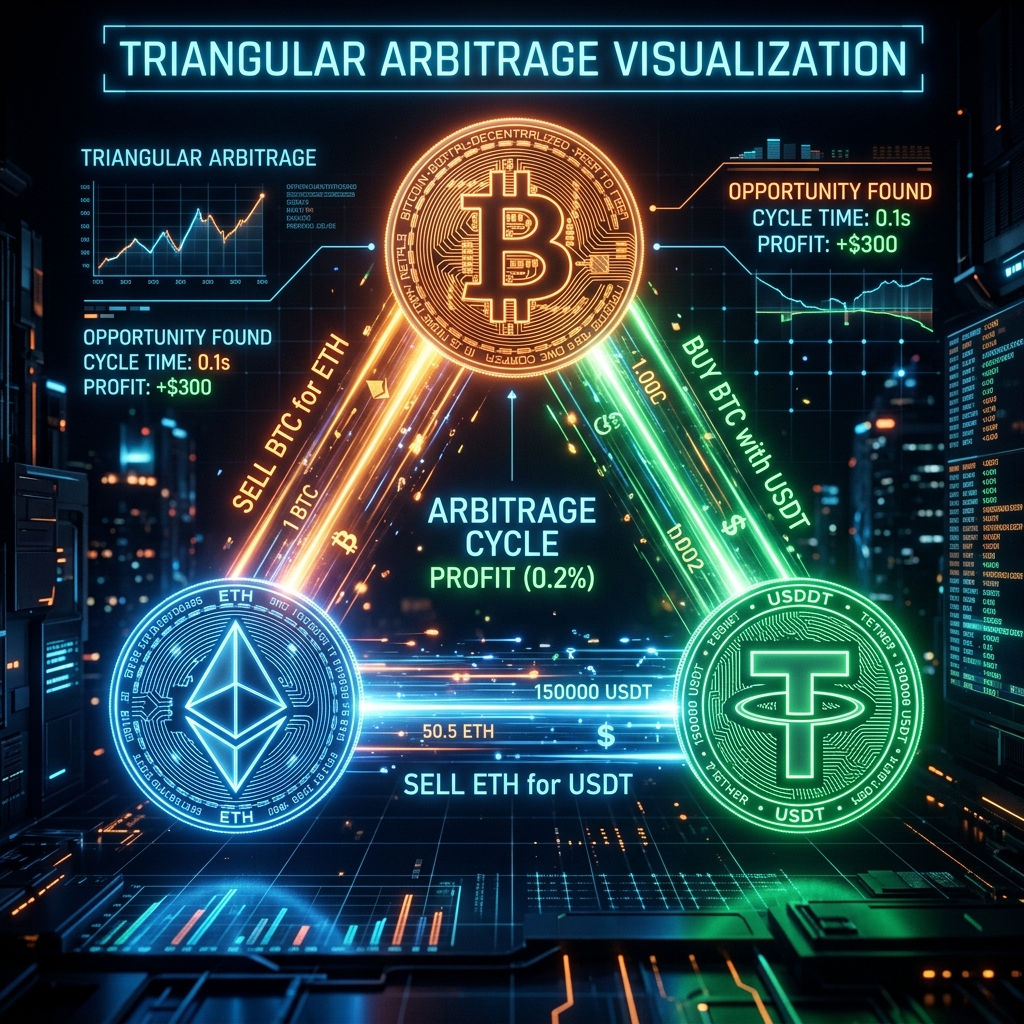

Imagine you have $10,000 USDT. Let's look at a hypothetical pricing anomaly on a major exchange:

- Leg 1 (USDT -> BTC): You buy Bitcoin with your USDT. Let's say 1 BTC = $50,000. You get 0.20 BTC.

- Leg 2 (BTC -> ETH): You use that BTC to buy Ethereum on the BTC/ETH pair. Let's say the orderbook is slightly out of sync and 1 BTC buys 20 ETH. You get 4.00 ETH.

- Leg 3 (ETH -> USDT): You immediately sell that ETH back to USDT on the ETH/USDT pair. If 1 ETH is trading at $2,505, your 4.00 ETH sells for $10,020 USDT.

You started with $10,000. You ended with $10,020. You made $20 (0.2%) in less than a second, taking zero directional market risk.

The Execution Challenge: The Speed of Light

If Triangular Arbitrage is risk-free, why isn't everyone doing it? Because the anomaly only exists for milliseconds. As soon as an imbalance occurs, High-Frequency Trading (HFT) bots detect it and execute the three-legged trade, instantly neutralizing the inefficiency.

To successfully execute TriArb, your algorithm needs three things:

- Colocation: Your servers must be physically located in the same data center as the crypto exchange to achieve microsecond latency.

- Atomic Execution: All three orders must be fired simultaneously or sequentially with guaranteed fills. If Leg 1 executes but Leg 2 fails due to slippage (the price moved), you are left holding unwanted directional risk (this is known as Execution Risk).

- Fee Optimization: A 0.2% profit is useless if the exchange charges 0.1% per trade (0.3% total fees). TriArb algorithms are only run by institutional market makers who have zero-fee or negative-fee (rebate) tier accounts.

Conclusion

Triangular Arbitrage is a perfect example of how quantitative algorithms act as the "janitors" of the financial markets. By ruthlessly exploiting pricing inefficiencies, these algorithms ensure that exchange rates remain perfectly balanced across thousands of interconnected trading pairs.