The Black-Scholes Illusion

Since 1973, the Black-Scholes-Merton model has been the holy grail of options pricing. It assumes that market volatility is constant across all strike prices and expiration dates. However, after the 1987 Black Monday crash, traders realized this was a fatal mathematical illusion. Deep out-of-the-money put options suddenly became incredibly expensive because traders were terrified of another crash.

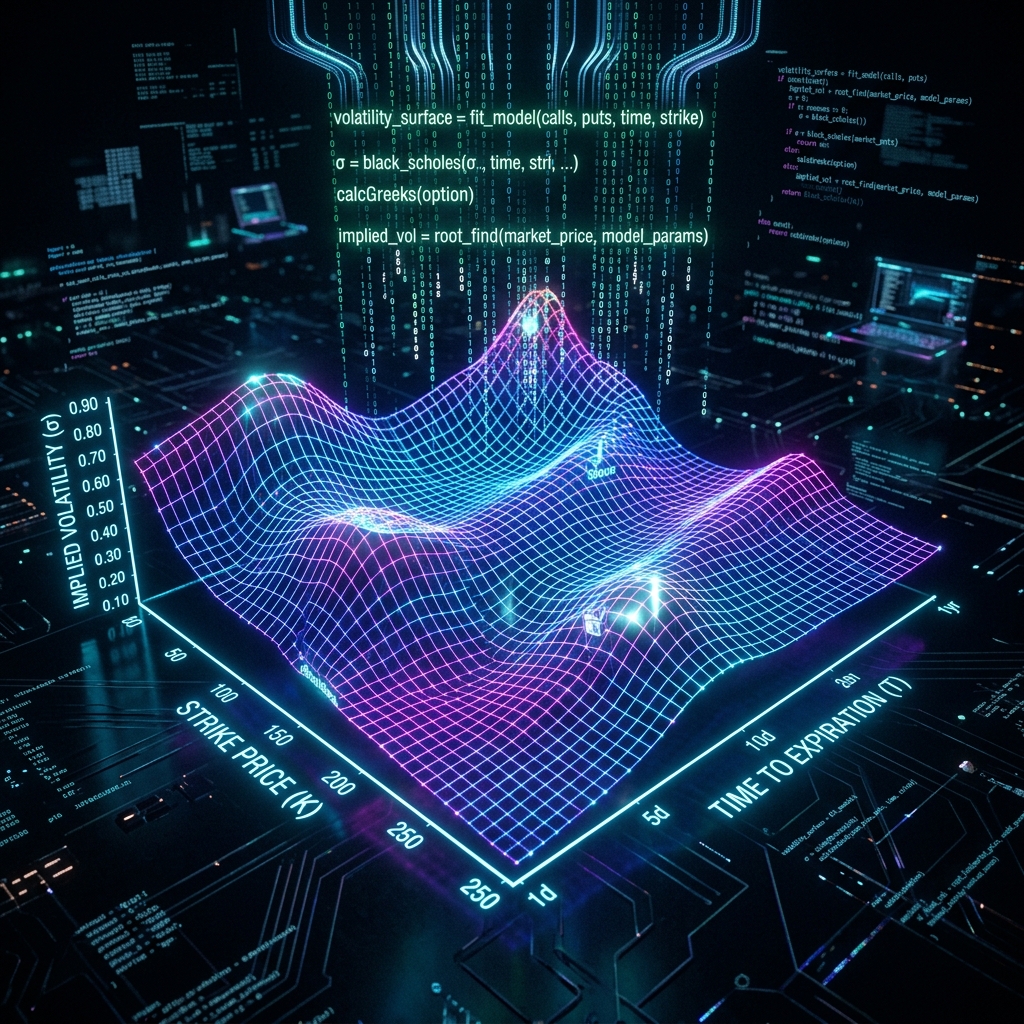

This fear broke the Black-Scholes equation and birthed the Implied Volatility (IV) Smile and the 3-dimensional Volatility Surface. The geometry of this surface dictates the true price of risk, but mapping it in real-time is a computationally massive problem.

Deep Learning the Topology of Risk

Traditional quants use complex stochastic calculus (like the Heston or SABR models) to estimate the Volatility Surface. These models are slow, require intense calibration, and often fail during extreme market stress.

The Neural Net Arbitrage

Modern algorithmic trading desks have replaced stochastic calculus with Deep Neural Networks (DNNs). The AI takes thousands of raw, fragmented options prices from the order book and instantly renders a perfect, continuous 3D mathematical surface.

Because the Neural Network can compute the surface in milliseconds—thousands of times faster than traditional SABR models—it creates a micro-arbitrage opportunity. If the AI detects that a specific options contract is priced below the "true" algorithmic surface (perhaps due to a momentarily sloppy human market maker), the AI instantly buys the cheap option and hedges the delta, locking in a mathematically guaranteed, risk-free profit.

The Local Volatility Neural PDE

The bleeding edge of this technology involves using Neural Networks to solve Partial Differential Equations (PDEs). By creating a "Physics-Informed Neural Network" (PINN), quants force the AI to respect the fundamental laws of arbitrage-free pricing.

This allows the algorithm to price highly complex "Exotic Options" (like Barrier or Asian options) instantaneously, a task that traditionally required overnight Monte Carlo simulations on massive server farms.

Conclusion

In the derivatives market, speed and mathematical precision are everything. By utilizing Deep Learning to instantly map and navigate the complex, multi-dimensional topography of the Volatility Surface, elite algorithmic systems can exploit pricing anomalies invisible to human traders and traditional mathematical models.